Malawian households are borrowing to put food on the table and meet everyday expenses, with village banks, neighbours and relatives serving as the country’s biggest lenders, a National Statistical Office (NSO) survey has established.

Findings from the NSO Sixth Integrated Household Survey (IHS6) published on Friday show that consumption accounts for 55 percent of all loans obtained by households, far outstripping borrowing for business capital at 11 percent and household non-farm expenditure at 14.9 percent.

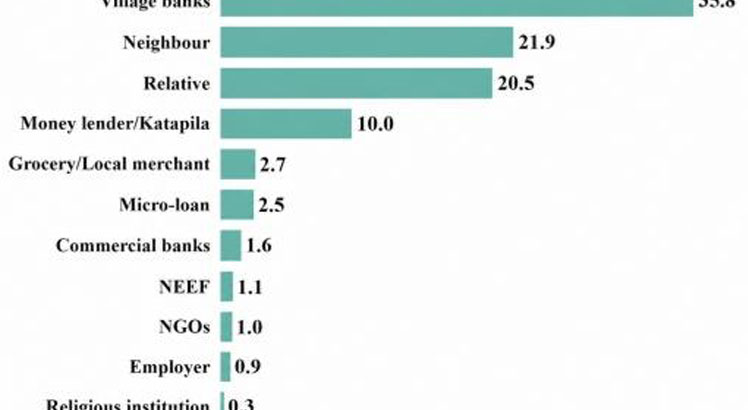

The data further show that household borrowing in Malawi is primarily sourced from informal and community-based channels with village banks accounting for 35.8 percent of all loans, followed by neighbours at 21.9 percent and relatives at 20.5 percent.

Reads the report: “The Southern Region has the highest proportion of loans designated for consumption at 59.8 percent and the lowest proportion for agricultural inputs for food crops at 5.5 percent.

“The Central Region records higher proportions for agricultural inputs for food crops at 10.8 percent and business start-up activities at 5.8 percent.”

The report further said the Northern Region records higher proportions for inputs related to tobacco at 2.8 percent and household non-farm expenditure at 20.2 percent, with a comparatively lower consumption share of 44.6 percent.”

About 65.1 percent of all loans fall within the K10 000 to K50 000 range while 21.4 percent are below K10 000 and only 13.5 percent exceed K50 000, according to the NSO.

Ironically, 54.6 percent of households interacted with the credit market during the 12 months preceding the survey, highlighting the growing role of borrowing in helping families manage economic pressures.

At national level, 40.1 percent of households with loans have not fully repaid them due to financial constraints cited by 38.9 percent of households.

In the previous survey, NSO found that village banks were gradually becoming the main source of borrowing for households nationwide.

NSO figures at the time showed that about 42.1 percent of the households borrowed from village banks while 15.1 percent borrow from relatives, 12.7 percent from neighbours, nine percent from loan sharks (katapila) and 6.1 percent from other sources.

In its Malawi Economic Monitor for July 2025, the World Bank also reported that village banks emerged as the primary source of borrowing for most Malawians seeking to support food consumption amid growing financial hardship and limited access to formal financial services.

Minister of Finance, Economic Planning and Decentralisation Joseph Mwanamvekha noted in an accompanying statement of the report that the data collection initiative, undertaken every three to four years, encompasses a range of subjects and is instrumental in informing national policies and development strategies.

In an interview yesterday, Consumers Association of Malawi executive director John Kapito said “village banks have grown over time due to several factors, including trust and tailored lending conditions that are attractive to local communities”.